Beranda

/ How To Compute Beginning Inventory - Applying And Analyzing Inventory Costing Methods / If you purchased $2,000 more in inventory, your figure would be $2,700.

How To Compute Beginning Inventory - Applying And Analyzing Inventory Costing Methods / If you purchased $2,000 more in inventory, your figure would be $2,700.

Insurance Gas/Electricity Loans Mortgage Attorney Lawyer Donate Conference Call Degree Credit Treatment Software Classes Recovery Trading Rehab Hosting Transfer Cord Blood Claim compensation mesothelioma mesothelioma attorney Houston car accident lawyer moreno valley can you sue a doctor for wrong diagnosis doctorate in security top online doctoral programs in business educational leadership doctoral programs online car accident doctor atlanta car accident doctor atlanta accident attorney rancho Cucamonga truck accident attorney san Antonio ONLINE BUSINESS DEGREE PROGRAMS ACCREDITED online accredited psychology degree masters degree in human resources online public administration masters degree online bitcoin merchant account bitcoin merchant services compare car insurance auto insurance troy mi seo explanation digital marketing degree floridaseo company fitness showrooms stamfordct how to work more efficiently seowordpress tips meaning of seo what is an seo what does an seo do what seo stands for best seotips google seo advice seo steps, The secure cloud-based platform for smart service delivery. Safelink is used by legal, professional and financial services to protect sensitive information, accelerate business processes and increase productivity. Use Safelink to collaborate securely with clients, colleagues and external parties. Safelink has a menu of workspace types with advanced features for dispute resolution, running deals and customised client portal creation. All data is encrypted (at rest and in transit and you retain your own encryption keys. Our titan security framework ensures your data is secure and you even have the option to choose your own data location from Channel Islands, London (UK), Dublin (EU), Australia.

How To Compute Beginning Inventory - Applying And Analyzing Inventory Costing Methods / If you purchased $2,000 more in inventory, your figure would be $2,700.. Subtract beginning inventory from ending inventory. Purchases refer to the additional merchandise added by a retail. Add up the purchased inventory with the beginning inventory to calculate the total inventory that is available during the period. Beginning inventory of finished goods; To calculate the ending inventory, use the following formula.

Multiply your ending inventory balance with the production cost of each item. Next subtract the amount of inventory that was purchased since the balance sheet was recorded. An example of the gross profit method. Beginning inventory of finished goods; Beginning inventory is also a good way to determine average inventory for your accounting periods — you can add the beginning inventory for many accounting periods together and divide by the number of accounting periods you used to get a rough idea of how much inventory you have in stock, on average.

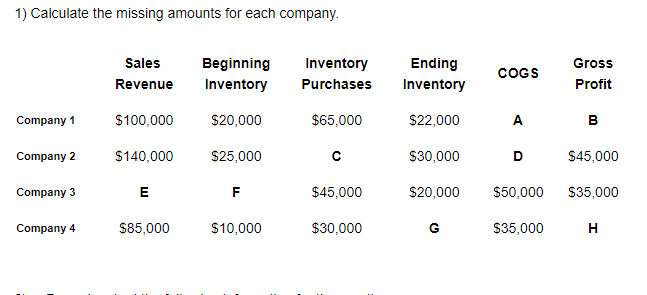

1 Calculate The Missing Amounts For Each Company Chegg Com from media.cheggcdn.com Take the number from the balance sheet as your starting point. Add up the purchased inventory with the beginning inventory to calculate the total inventory that is available during the period. The cost of goods sold includes the total cost of purchasing inventory. They then apply this figure to whichever cost flow assumption the business chooses to use, whether fifo, lifo or the weighted average. Cost of goods sold (cogs) cogs is the inventory value sold for a given accounting period. If we return to our example, then the calculation will be as follows: Do the same with the amount of new inventory. Calculate the cost of goods available for sale.

The primary use of beginning inventory is to serve as the starting point of the cost of goods sold calculation for an accounting period, for which the calculation is:

You calculate and record beginning inventory so that you can calculate ending inventory. The cost of goods sold includes the total cost of purchasing inventory. Say your online store has a beginning inventory value of $175,000 in january. Subtract beginning inventory from ending inventory. $30,000 + $14,000 = $44,000 subtract the ending inventory from the total inventory to determine the cost of goods sold. Cost of goods manufactured (cogm) cost of goods sold (cogs) all three of these are used in the finished goods inventory formula. The basic formula for calculating ending inventory is: If you purchased $2,000 more in inventory, your figure would be $2,700. Therefore, in order to compute the final balance of the raw materials, take up the beginning balance of the raw materials. Thus, the steps needed to derive the amount of inventory purchases are: To calculate the ending inventory, use the following formula. Next, add the cost of any new purchases added to the business during the current accounting period. While this is true, there are two.

Add the cost of goods sold to the difference between the ending and beginning inventories. Say your online store has a beginning inventory value of $175,000 in january. While beginning and ending inventory are necessary to compute cost of goods sold, they may or may not appear on an income statement. Cost of good available for sale = cost of beginning inventory + cost of purchases. Subtract the estimated cost of goods sold from the cost of goods available for sale;

Calculate The Inventory Turnover For Supplies For The Nursing Department 900 000 Beginning Inventory 300 000 Ending Inventory Homeworklib from img.homeworklib.com Subtract the estimated cost of goods sold from the cost of goods available for sale; Multiply the gross profit percentage by sales in the period; However, if you have no clear inventory records, you can use the formula below to calculate the starting inventory. Cost of good available for sale = cost of beginning inventory + cost of purchases. When calculating the cost of goods sold, whether as a retailer or a manufacturer, opening inventory is a fundamental part of the equation. How to calculate your beginning inventory after determining the ending inventory balance and cogs from the previous accounting period, you can now calculate your beginning inventory at the start of a new accounting period. The beginning inventory for a financial year is the ending inventory for the previous financial year. Where, beginning inventory is the inventory of goods that were not sold and were leftover in the previous financial year.

Obtain the total valuation of beginning inventory, ending inventory, and the cost of goods sold.

Calculate the cost of goods sold: If we return to our example, then the calculation will be as follows: The formula for doing so is: The cost of goods sold includes the total cost of purchasing inventory. This formula for cogs calculation applies to the retail companies. They then apply this figure to whichever cost flow assumption the business chooses to use, whether fifo, lifo or the weighted average. Beginning inventory and purchases are the input that accountants use to calculate the cost of goods available for sale. Next, add the cost of any new purchases added to the business during the current accounting period. The primary use of beginning inventory is to serve as the starting point of the cost of goods sold calculation for an accounting period, for which the calculation is: Add the cost of goods sold to the difference between the ending and beginning inventories. Therefore, in order to compute the final balance of the raw materials, take up the beginning balance of the raw materials. Cost of goods sold (cogs) cogs is the inventory value sold for a given accounting period. The net purchases are the items you've bought and added to your inventory count.

How to calculate beginning inventory of finished goods is the same as calculating ending finished goods. Next, deduct the raw materials that are utilized for either work in process or in the finished items inventory. It's acceptable accounting practice to combine raw materials, works in progress and finished goods into a single balance sheet asset account. This formula for cogs calculation applies to the retail companies. Obtain the total valuation of beginning inventory, ending inventory, and the cost of goods sold.

First In First Out Fifo Method In Periodic Inventory System Accounting For Management from www.accountingformanagement.org Cost of goods sold (cogs) cogs is the inventory value sold for a given accounting period. Obtain the total valuation of beginning inventory, ending inventory, and the cost of goods sold. Cost of goods manufactured (cogm) cost of goods sold (cogs) all three of these are used in the finished goods inventory formula. Beginning inventory and purchases are the input that accountants use to calculate the cost of goods available for sale. Multiply the gross profit percentage by sales in the period; Therefore, in order to compute the final balance of the raw materials, take up the beginning balance of the raw materials. The cost of goods sold includes the total cost of purchasing inventory. The average inventory is calculated by adding the inventory at the beginning of the period to the inventory at the end of the period and dividing by two.

Next, add the cost of any new purchases added to the business during the current accounting period.

If, say, you're making out your balance sheet, you'll need to include inventory levels as an asset. Formula to calculate cost of goods sold (cogs) the formula to calculate the cost of goods sold is: Next subtract the amount of inventory that was purchased since the balance sheet was recorded. Cost of goods sold (cogs) cogs is the inventory value sold for a given accounting period. With proper inventory management, opening inventory is the same as the ending inventory for the last accounting period. The basic formula for calculating ending inventory is: Obtain the total valuation of beginning inventory, ending inventory, and the cost of goods sold. Obtain the total valuation of beginning inventory, ending inventory, and the cost of goods sold. Where, beginning inventory is the inventory of goods that were not sold and were leftover in the previous financial year. Your beginning inventory is the last period's ending inventory. When calculating the cost of goods sold, whether as a retailer or a manufacturer, opening inventory is a fundamental part of the equation. Add up the purchased inventory with the beginning inventory to calculate the total inventory that is available during the period. Beginning inventory of finished goods;

When calculating the cost of goods sold, whether as a retailer or a manufacturer, opening inventory is a fundamental part of the equation how to compute inventory. Subtract the estimated cost of goods sold from the cost of goods available for sale;